Category: Blog

-

When Clients Have Global Ties: U.S. Estate Planning Issues for Cross-Border Clients

Who among us does not have clients with ties to another country? These international connections often raise special considerations in estate planning. This article offers an overview of key U.S. estate tax rules that apply when clients have cross-border ties, while putting aside, for now, the related (and complex) topics of gift tax, income tax,…

-

Why Family Business Succession Issues Break Estate Plans

Estate plans for business owners rarely fail because of poor drafting. They fail when the documents are sound but the situation is not.They fail when the plan is built on assumptions no one tested. This is especially common in estate planning for family business owners, where the success of the plan often depends on how…

-

Number One Factor to Successful Financial Planning

Regardless of what financial or estate planning strategy is considered, and whether the goal is to protect wealth from creditor claims, minimize income tax or reduce estate and gift tax, there is one factor that is the heart of the most successful outcomes. And that is the return on the investments or assets used in the strategy. Take…

-

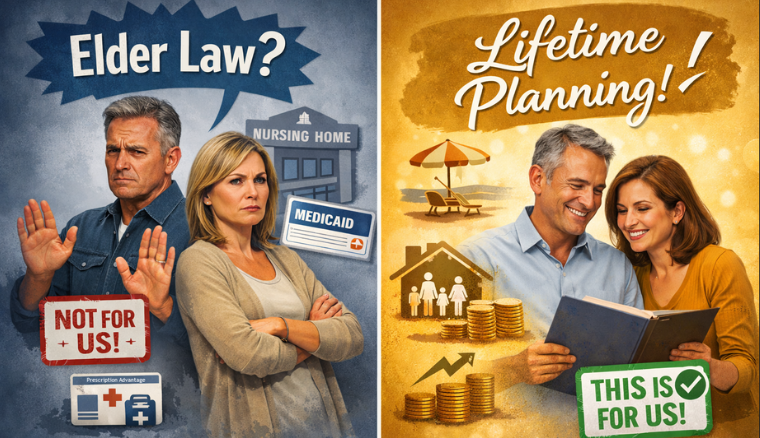

Elder Law Has a Branding Problem—And It’s Costing You Clients

If you work in or around the elder law space, you’ve probably felt it: a quiet resistance from prospective clients who should be a perfect fit—but don’t quite see themselves in what you do. They hesitate. They delay. Or worse, they only show up when something has already gone wrong. And while there are many…

-

Getting In Front of New Clients: Don’t Let AI Eat Your Lunch!

The greatest risk to estate planning attorneys today isn’t that AI will replace them. It’s that clients will believe it can. With platforms like Trust & Will, LegalZoom, and even ChatGPT offering “quick and cheap” solutions, many potential clients are being lulled into thinking estate planning is nothing more than filling in blanks on a…

-

Stuck in the Middle: The Ethics of Representing Couples in Estate Planning

The joint representation of couples in estate planning presents a unique set of ethical challenges and considerations for attorneys. Whether dealing with married or unmarried couples, or even other related family members, lawyers must navigate the delicate balance between confidentiality, conflicts of interest, and the best interests of each client. This blog post explores these…

-

Death, Taxes, Certainty, and Uncertainty

The saying that the only things that are certain are death and taxes is attributed to Benjamin Franklin. There are other certainties of course, but for attorneys like me who think about estate taxation, death and taxes are a daily focus. And right now, while those things are certain, the tax laws themselves are arguably…

-

Estate Planning for Mid-Net Worth Families: A Guide in Blog Form

For many Americans, estate planning is perceived as a concern primarily for the very wealthy. However, mid-net worth families—those who may not be subject to federal estate taxes but still have significant assets to protect—need careful planning to ensure their legacies are preserved and passed on according to their wishes. This blog explores effective estate…

-

Navigating the SECURE Act: Implications for Estate Planning with Retirement Accounts

The enactment of the Setting Every Community Up for Retirement Enhancement (SECURE) Act in December 2019 marked a significant shift in the landscape of retirement and estate planning. This legislation introduced changes that affect how retirement accounts are managed after the account holder’s death, specifically altering the distribution rules that estate planners have relied upon…

-

Estate Planning is Not Easy

“Over my career, I have found that some people view estate planning as one of the easier areas of law to practice. Attorneys who work in this area know the reality, however – estate planning is not easy. “ Clients Think Estate Planning is Easy I practiced for 17 years doing estate plans for all levels…